Printable Schuldentagebuch

Schulden verfolgen und mit einer klaren Tilgungsstrategie abbauen

Track every debt, interest rate, and payment in one structured table. Log your creditor, debt type, and chosen payoff strategy — snowball or avalanche — to stay organized and accelerate your path to financial freedom.

Felder anpassen

Schalten Sie Felder ein oder aus. Klicken Sie auf den Stift zum Umbenennen oder fügen Sie eigene Felder hinzu.

Vorteile

Anleitung

Was ist dieses Journal?

A debt journal is a structured tracking tool for anyone working to pay off loans, credit cards, or other financial obligations. By recording each creditor, debt type, total owed, interest rate, minimum payment, actual payment made, remaining balance, and your chosen payoff method, you maintain complete visibility over your debt landscape. This journal transforms the often overwhelming experience of carrying multiple debts into a clear, manageable action plan.

Debt payoff is as much a psychological challenge as a financial one. Seeing your balances decrease — even by small amounts — provides the motivation to keep going. This journal supports popular payoff strategies like the debt snowball (paying off smallest balances first for quick wins) and debt avalanche (tackling highest interest rates first for mathematical efficiency), helping you stay committed to whichever approach suits your personality and situation.

Whether you are managing student loans, a mortgage, credit card balances, medical bills, or personal loans, this journal keeps every obligation organized in one place. It is particularly powerful when paired with a budget journal, as together they ensure that every extra dollar is strategically directed toward your most impactful debt, accelerating your path to financial freedom.

Ausgefülltes Beispiel

So sieht ein typischer Eintrag aus, wenn er ausgefüllt ist:

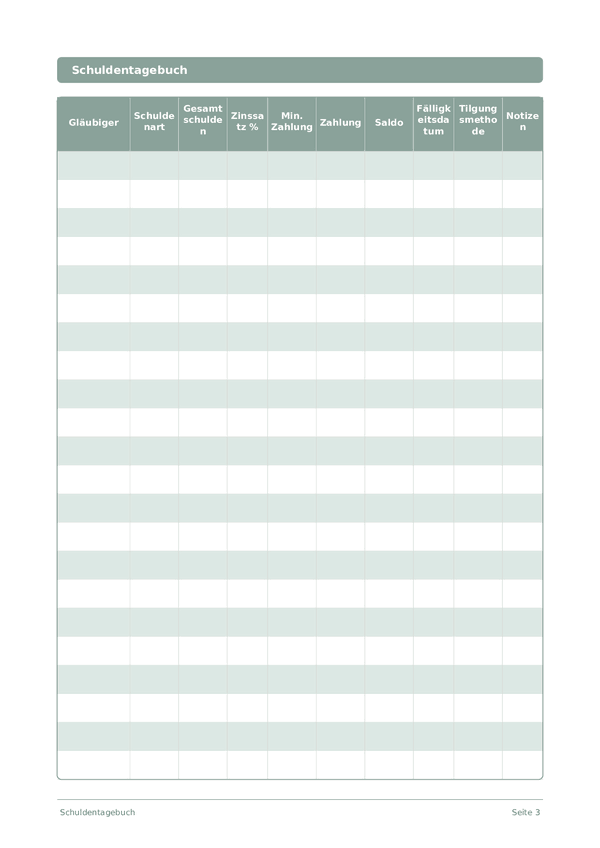

| Gläubiger | Schuldenart | Gesamtschulden | Zinssatz % | Min. Zahlung | Zahlung | Saldo | Fälligkeitsdatum | Tilgungsmethode | Notizen |

|---|---|---|---|---|---|---|---|---|---|

| Chase Visa | Credit card | 4200 | 22.99 | 84 | 350 | 3850 | 2026-03-15 | Avalanche | Highest interest — priority target |

| Sallie Mae | Student loan | 18500 | 5.5 | 195 | 195 | 18305 | 2026-03-28 | Standard | Federal loan, income-driven repayment |

| Toyota Financial | Auto loan | 12800 | 4.25 | 310 | 310 | 12490 | 2026-03-20 | Standard | 24 months remaining |

| Capital One | Credit card | 1150 | 19.99 | 35 | 200 | 950 | 2026-03-10 | Snowball | Smallest balance — close to payoff! |

| City Hospital | Medical bill | 2400 | 0 | 100 | 100 | 2300 | 2026-03-25 | Standard | 0% interest payment plan, 24 months |

Wie Sie jedes Feld ausfüllen

Jede Seite ist eine Tabelle mit Spalten. Füllen Sie pro Eintrag eine Zeile aus. Hier erfahren Sie, wofür jede Spalte gedacht ist:

Gläubiger

Schuldenart

Gesamtschulden

Zinssatz %

Min. Zahlung

Zahlung

Saldo

Fälligkeitsdatum

Tilgungsmethode

Notizen

Fügen Sie zusätzlichen Kontext oder Gedanken hinzu. Diese Auffangspalte ist für alles, was nirgendwo anders hinpasst, aber später nützlich sein könnte.

Tipps für den Erfolg

Wann und wie oft schreiben

Update your debt table every time you make a payment — capturing the new balance, amount paid, and any extra above the minimum. At minimum, this happens monthly with regular payment cycles. Weekly, spend 5 minutes reviewing upcoming due dates to avoid late fees. Monthly, recalculate your total debt, total interest paid, and debt-to-income ratio. Celebrate each debt fully paid off with a journal entry reflecting on what you learned and how it felt.

Häufig gestellte Fragen

Wie unterscheiden sich Snowball und Avalanche in der Spalte tilgungsmethode?

Snowball sortiert Schulden nach kleinstem Saldo zuerst; Avalanche nach höchster zinssatz % zuerst. Dave Ramsey populrisierte Snowball in 'The Total Money Makeover' (Thomas Nelson, 2003) für den Verhaltensimpuls. Avalanche minimiert mathematisch die gesamten Zinsen. Das CFPB (2023, 'How to Pay Off Credit Card Debt') (in Deutschland: Verbraucherzentrale, BaFin) beschreibt beide als legitime Strategien; die Spalte tilgungsmethode ermöglicht es, pro Gläubiger eine Wahl zu markieren und einzuhalten.

Wie fülle ich die Spalte zinssatz % korrekt aus?

Verwenden Sie den effektiven Jahreszins (APR/Effektivzinssatz) aus Ihrer Abrechnung, nicht den Monatszins. Das CFPB (2023, 'What is a credit card interest rate?') definiert APR als die standardisierten jährlichen Kreditkosten. Tragen Sie dieselbe Form für jeden Gläubiger ein, damit Vergleiche gültig sind. Bei variablen Karten aktualisieren Sie die Spalte bei jeder Zinsänderung - typischerweise nach Schritten der Federal Reserve oder EZB.

Warum enthält das Journal sowohl min. Zahlung als auch payment?

Min. Zahlung ist das, was der Gläubiger verlangt; payment ist das, was Sie tatsächlich zahlen. Das CFPB (2022, 'Making Minimum Payments on Credit Cards') warnt, dass nur die Mindestzahlung die Rückzahlung um Jahre verlängert und die Gesamtzinsen verdoppeln kann. Das parallele Verfolgen beider Spalten zeigt die Lücke und motiviert, payment wann immer möglich zu erhöhen, um die Tilgung zu beschleunigen.

Ist die Avalanche-Methode wirklich mathematisch besser?

Avalanche minimiert mathematisch die Gesamtzinsen, weil sie zuerst die höchste zinssatz % angreift. Das CFPB (2023, 'How to Pay Off Credit Card Debt') stellt fest, dass beide Methoden funktionieren und die Wahl davon abhängt, ob Sie Motivation oder Ersparnis brauchen. Snowball gewinnt oft verhaltensmässig bei Menschen, die frühe Erfolge brauchen, um konsistent zu bleiben - notieren Sie Ihre Methode und halten Sie sie ein.

Wie verfolge ich den laufenden Saldo über mehrere Seiten?

Nutzen Sie die Spalte balance nach jeder Zahlung: vorheriger Saldo minus payment, plus während des Zeitraums aufgelaufene Zinsen. Das CFPB (2023, 'Understanding Your Credit Card Statement') erklärt, wie Zinsen jedem Zyklus zur unbezahlten Hauptforderung hinzugefügt werden. Mit 15 Zeilen pro Seite planen Sie einen Gläubiger pro Zeile über den Monat; übertragen Sie den Endsaldo in den Eröffnungseintrag der nächsten Seite.

Was ist der häufigste Fehler beim Start eines Schuldenjournals?

Das Auslassen kleinerer Schulden. Das CFPB (2022, 'Debt Collection') (in Deutschland: Verbraucherzentrale) empfiehlt, jede Verpflichtung aufzulisten - medizinische, Ratenkarten, Privatkredite, Familiendarlehen - weil versteckte Schulden jeden Plan entgleisen lassen. Füllen Sie die Spalte creditor für jeden Saldo über null aus, auch wenn min. Zahlung klein ist. Die 15-Zeilen-Seite fasst das vollständige Schuldenbild der meisten Haushalte auf einem Blatt.

Hilft das Aufschreiben von Schulden tatsächlich der Tilgungsmotivation?

Ja, sichtbarer Fortschritt ist ein dokumentierter Verhaltenshebel. Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) beschreiben schriftliches Tracking als Selbstverpflichtungsmechanismus, der die Konsequenz erhöht. Das CFPB (2022, 'Tools for Tracking Your Money') befürwortet schriftliche Protokolle zur Verhaltensänderung. Das Beobachten, wie die Spalte balance Zeile für Zeile sinkt, liefert die Feedbackschleife, die abstrakte Ziele in nachhaltiges Handeln verwandelt.

Soll ich meine Hypothek in dieses Journal aufnehmen?

Optional - die meisten Snowball/Avalanche-Praktizierenden schliessen Hypotheken aus, weil die Zeitskala anders ist. Dave Ramsey, 'The Total Money Makeover' (Thomas Nelson, 2003) behandelt das Eigenheim als separate spätere Phase. Verwenden Sie die Spalte schuldenart, um 'Hypothek' zu markieren, und entscheiden Sie. Beim Ausschluss konzentrieren Sie die 15 Zeilen auf Kreditkarten, Autokredite, Studienkredite und Privatkredite, wo hohe zinssatz % schnellere Tilgung wirkungsvoll macht.

Das könnte Ihnen auch gefallen

Ausgabentagebuch

Jeden Euro verfolgen und die Kontrolle über Ihre Finanzen übernehmen

Investitionstagebuch

Trades verfolgen, Entscheidungen analysieren und Ihr Portfolio aufbauen

Spartagebuch

Tägliche Spargewohnheiten verfolgen und auf Ihre finanziellen Ziele hinarbeiten

Karrieretagebuch

Erfolge verfolgen und berufliches Wachstum täglich beschleunigen

Scrollen zum Zoomen, ziehen zum Bewegen