Printable Budget Journal

Track spending, compare plans, and reach savings goals

Take control of your finances with a structured monthly budget planner. List your spending categories, set planned amounts, and record actual expenses to see where your money really goes. With columns for the difference and payment method, you can identify overspending, cut unnecessary costs, and build a savings habit month after month.

Customize fields

Toggle fields on or off. Click the pencil to rename, or add your own fields.

Benefits

How to Use

What is this journal?

A budget journal is a monthly planning and tracking tool that helps you allocate your income across spending categories and monitor how actual expenses compare to your plan. Each page includes space for your total income and savings goal at the top, followed by a detailed breakdown of categories with planned amounts, actual spending, and the difference between them. This journal is for anyone who wants to move beyond vague budgeting intentions to concrete financial discipline.

Budgeting without tracking is like dieting without a scale — you may have good intentions, but without measurement, you cannot know if you are making progress. This journal provides the measurement framework. By reviewing the difference column at the end of each month, you immediately see which categories ran over or under budget, enabling data-driven adjustments for the following month. Over time, your budget becomes increasingly accurate and your spending becomes more aligned with your true priorities.

Whether you follow the 50/30/20 rule, zero-based budgeting, or your own custom system, this journal adapts to your approach. It is particularly valuable during major financial transitions — starting a new job, paying for education, buying a home, or building an emergency fund — when careful allocation of every dollar or ruble truly matters.

Filled example

Here's what a typical entry looks like when filled in:

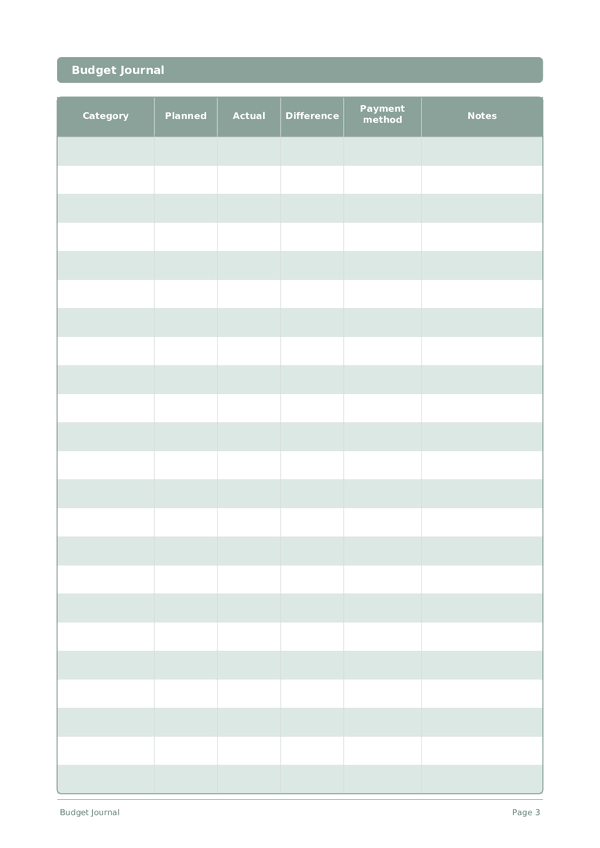

| Category | Planned | Actual | Difference | Payment method | Notes |

|---|---|---|---|---|---|

| Housing (rent/mortgage) | 1500 | 1500 | 0 | Bank transfer | Fixed monthly payment |

| Groceries & food | 600 | 645 | -45 | Debit card | Hosted dinner party mid-month |

| Transportation | 350 | 310 | 40 | Mixed | Biked to work 3 days — saved on gas |

| Utilities & internet | 180 | 195 | -15 | Auto-pay | Heating bill higher due to cold snap |

| Entertainment | 200 | 155 | 45 | Credit card | Stayed in most weekends |

How to fill in each field

Each page is a table with columns. Fill in one row per entry. Here's what each column is for:

Category

Assign a category to this entry (e.g., food, transport, entertainment). Consistent categories make your data easy to analyze.

Planned

Actual

Difference

Payment method

Notes

Add any additional context or thoughts. This catch-all column is for anything that doesn't fit elsewhere but might be useful later.

Tips for success

When and how often to write

Set up your budget on the 1st of each month: list all categories, planned amounts, and income. Then update actual spending daily or every other day — the shorter the delay, the more accurate your data. Do a mid-month checkpoint around the 15th to see if any category is already at 70%+ of its limit. At month-end, calculate every difference, note what worked, and carry forward adjustments into next month’s plan.

Frequently Asked Questions

How do the planned and actual columns work together?

Planned is set at the start of the month; actual is filled as you spend. The CFPB (2023, 'Your Money, Your Goals: Tracking Your Income and Expenses') describes this plan-versus-actual loop as the core budgeting discipline. The difference column then surfaces overspending category by category. Without recording planned first, the journal becomes a passive expense log instead of a budgeting tool.

What categories should I list in the category column?

Match real spending, not aspiration. The U.S. Bureau of Labor Statistics (2023, Consumer Expenditure Survey) groups household spending into categories like housing, food, transportation, healthcare, and entertainment as reasonable starting points. Customize from your last bank statement. Eighteen rows per page fit most households' detailed categories; very fine categories obscure the patterns the journal exists to reveal.

Should I use 50/30/20 or zero-based budgeting with this template?

Either works — choose by temperament. The 50/30/20 rule comes from Elizabeth Warren & Amelia Warren Tyagi, 'All Your Worth' (Free Press, 2005): 50% needs, 30% wants, 20% savings. Zero-based budgeting traces to Peter Pyhrr, 'Zero-Base Budgeting' (Harvard Business Review, Nov–Dec 1970): every dollar planned to a category. The journal supports both because the planned column accepts any allocation method.

Why does the journal include a payment method column?

Different payment methods correlate with different spending patterns. Prelec & Simester (2001, Marketing Letters, 12(1), 5–12) found willingness to pay rises markedly with credit cards versus cash. Hirschman (1979, Journal of Consumer Research, 6(1), 58–66) documented similar effects. Tagging payment method makes that behavior visible; over months you may see categories where credit spending consistently exceeds plan.

What goes in the income and savings goal page headers?

Net monthly income — what actually arrives in your account — and a specific savings target for the month. The CFPB (2023, 'Setting Savings Goals') emphasizes specific, time-bound savings goals over vague intent. Filling these headers anchors every category planned amount; if planned amounts sum above income minus savings goal, the math fails before the month begins.

How is this different from Mint, YNAB, or other apps?

Apps automate transaction capture; paper enforces conscious entry. Soman (2001, Journal of Consumer Research, 27(4), 460–474) found manual recording of payments reduces subsequent spending — automation removes that friction. Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) describe written friction as a behavioral feature. Use both if helpful — app for completeness, journal for behavioral effect.

Does writing down a budget actually change spending?

Yes — mental and recorded budgeting both shift behavior. Heath & Soml (1996, Journal of Consumer Research, 23(1), 40–52) documented that explicit budget categories alter spending. The CFPB (2023, 'Your Money, Your Goals: Tracking Your Income and Expenses') endorses written tracking specifically. Filling planned then actual makes the gap visible row by row, the basic feedback loop behavior change requires.

What is the most common budgeting mistake this template prevents?

Setting planned amounts but never recording actual. The CFPB (2023, 'Your Money, Your Goals: Tracking Your Income and Expenses') notes plans without tracking produce no behavior change. The eighteen-row layout sized for monthly review forces both halves of the cycle. The difference column makes the consequence of unrecorded spending impossible to hide once you sit down weekly to update rows.

You Might Also Like

Scroll to zoom, drag to move