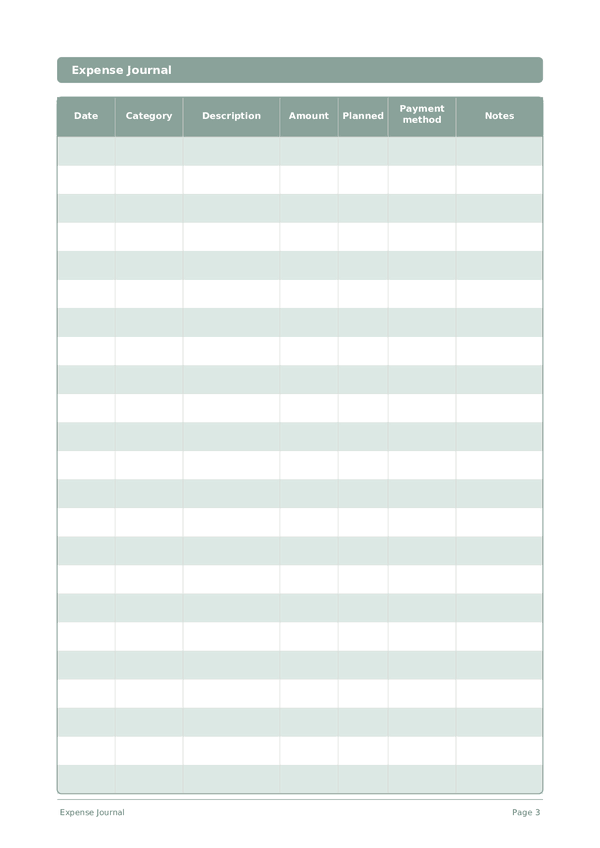

Printable Savings Journal

Track daily savings habits and build toward your financial goals

Log how much you save each day, track your running total, and rate your consistency streak. Research shows that daily tracking and visible progress are the two most powerful drivers of financial goal achievement — this template puts both in your hands.

Customize fields

Toggle fields on or off. Click the pencil to rename, or add your own fields.

Benefits

How to Use

What is this journal?

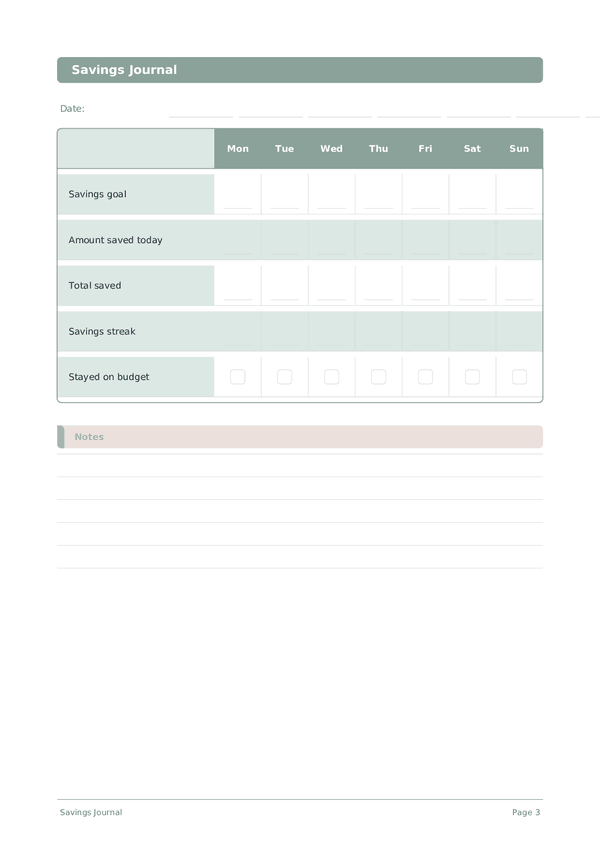

A Savings Journal is a weekly tracker designed to help you build consistent saving habits and watch your money grow over time. Each week, you log your savings goal, the amount you saved each day, your running total, whether you stayed on budget, and your current savings streak. This simple visual format makes it easy to spot trends and stay motivated.

Tracking your savings daily transforms an abstract financial goal into a concrete, manageable routine. Research in behavioral economics shows that people who monitor their finances regularly save significantly more than those who do not. By recording even small amounts, you reinforce the habit and build momentum.

Use this journal every evening as part of your wind-down routine. Fill in the amount you set aside today, check whether you stayed within your daily budget, and update your streak. Over weeks and months, the filled-in rows become a powerful visual reminder of your progress and discipline.

Filled example

Here's what a typical entry looks like when filled in:

| Mon | Tue | Wed | Thu | Fri | Sat | Sun | |

|---|---|---|---|---|---|---|---|

| Savings goal | 50 | 50 | 50 | 50 | 50 | 50 | 50 |

| Amount saved today | 50 | 30 | 50 | 45 | 60 | 25 | 50 |

| Total saved | 1250 | 1280 | 1330 | 1375 | 1435 | 1460 | 1510 |

| Savings streak | 5 | 0 | 1 | 2 | 3 | 0 | 1 |

| Stayed on budget | ✓ | ✓ | ✓ | ✓ | ✓ |

How to fill in each field

Each page is a weekly grid. Rows are your tracking items, columns are days of the week. Here's what each item means:

Savings goal

Amount saved today

Total saved

Savings streak

Stayed on budget

Tips for success

When and how often to write

Make a daily entry noting whether you saved anything today, even a small amount, and update your running total. The daily rhythm builds identity as a saver — it takes about 30 seconds. Weekly, review your consistency streak and total saved that week. Monthly, compare your actual savings rate to your target, check that your money is in the best available account, and adjust your daily or weekly target if needed.

Frequently Asked Questions

Why does this journal track daily savings rather than monthly totals?

Daily check-ins create habit consistency that monthly tallies miss. The CFPB (2022, 'Tools for Tracking Your Money') notes that frequent self-monitoring strengthens follow-through on financial goals. Recording amount saved today even on small days reinforces the behavior. Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) call this self-tracking a commitment device; daily entries make abstract savings goals concrete.

How do I use the single savings goal field most effectively?

Write one specific dollar target with a date, for example 'Emergency fund: $3,000 by December'. The CFPB (2023, 'Setting Savings Goals') recommends specific, measurable goals over vague intentions. The total saved field then becomes meaningful progress toward that single number. Avoid splitting attention across multiple goals on the same page; focus accelerates accumulation.

What does the savings streak rating actually measure?

Consistency, not amount. A rating of 10 means unbroken daily entries regardless of size; 1 means you just started or restarted. The CFPB (2022, 'Tools for Tracking Your Money') emphasizes consistency as the primary driver of savings success. Use the rating to reward showing up: even a $1 entry preserves your streak and the habit underlying it.

How much should I aim to save each day?

No fixed amount applies to everyone. The U.S. Bureau of Labor Statistics (2023, Consumer Expenditure Survey) shows household saving rates vary widely with income and stage of life. Use amount saved today to record what you actually set aside, however small. Consistency over months, visible in your growing total saved, outweighs any specific daily target.

Why include a stayed on budget checkbox in a savings journal?

Saving and spending are two sides of the same balance sheet. The CFPB (2022, 'Tools for Tracking Your Money') links budget adherence directly to saving capacity. Checking the box on disciplined days connects cause and effect: you see how budget control today fueled the amount saved today figure, reinforcing the relationship between spending decisions and goal progress.

Does writing down savings really lead to saving more?

Self-monitoring consistently outperforms intention alone in behavior-change research. Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) document that written tracking increases follow-through across financial behaviors. The CFPB (2022, 'Tools for Tracking Your Money') endorses written logs. The combination of amount saved today, total saved, and savings streak on this template covers all three reinforcement loops: input, accumulation, consistency.

How does this differ from a budgeting app like Mint or YNAB?

Apps automate transaction capture; this journal forces conscious entry. The friction is the feature: Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) explain that small effort raises attention. Writing amount saved today by hand, then watching total saved grow, engages reflection that auto-imports skip. Use both if helpful: the app for completeness, the journal for behavioral reinforcement.

What if I miss a day - should I break my savings streak?

Reset gently: rate the day low rather than abandoning the journal. The CFPB (2022, 'Tools for Tracking Your Money') stresses that consistency means returning, not perfection. Stephen Covey, 'The 7 Habits of Highly Effective People' (Free Press, 1989) frames recovery as part of the discipline. Resume the next day with even a small entry; preserved habits beat perfect-but-abandoned ones.

You Might Also Like

Scroll to zoom, drag to move