Printable Expense Journal

Track every dollar to take control of your finances

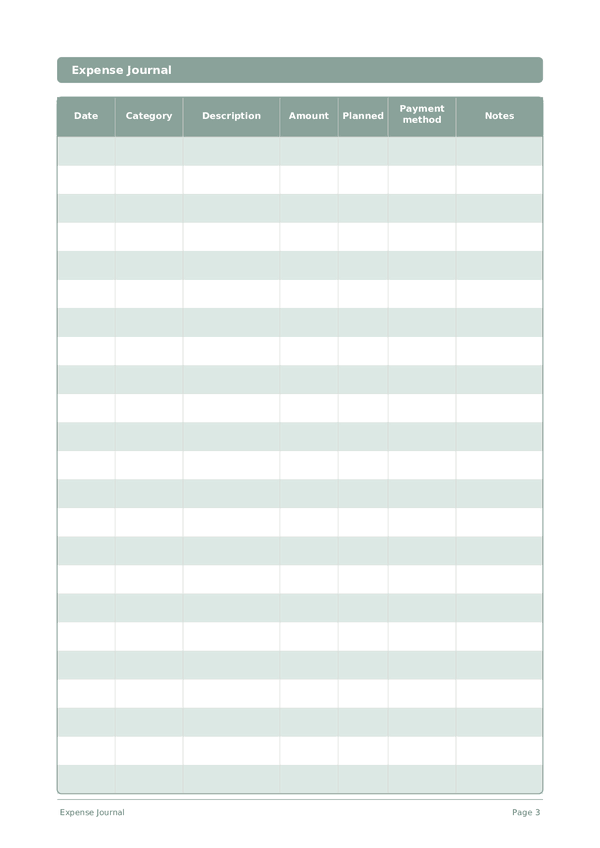

A daily expense log designed to capture every purchase with date, category, amount, and payment method. Compare planned budgets against actual spending, spot financial leaks, and build lasting money awareness. The simple table format makes it easy to fill in on the go and review at the end of each week or month.

Customize fields

Toggle fields on or off. Click the pencil to rename, or add your own fields.

Benefits

How to Use

What is this journal?

An expense journal is a straightforward daily log for tracking every purchase and expenditure you make. By recording the date, category, description, amount, and payment method for each transaction, you build complete visibility into where your money goes. This journal is designed for anyone who wants to take control of their spending — from students and young professionals to families managing household budgets.

Most people significantly underestimate their discretionary spending. Small daily purchases — coffee, snacks, subscriptions, impulse buys — add up to surprisingly large sums over a month. An expense journal makes these invisible costs visible. When you write down every transaction, you naturally become more intentional about your spending, and patterns emerge that help you identify areas where you can cut back without sacrificing quality of life.

This journal is also an excellent companion to budgeting. By comparing your actual expenses against planned amounts, you can see exactly where you are on track and where adjustments are needed. Whether you are saving for a specific goal, paying down debt, or simply building healthier financial habits, consistent expense tracking is the foundation of financial awareness and control.

Filled example

Here's what a typical entry looks like when filled in:

| Date | Category | Description | Amount | Planned | Payment method | Notes |

|---|---|---|---|---|---|---|

| 2026-03-03 | Groceries | Weekly grocery shopping at Whole Foods | 87.5 | 80 | Debit card | Slightly over budget, bought organic produce |

| 2026-03-03 | Transport | Gas fill-up | 52 | 50 | Credit card | Prices went up this week |

| 2026-03-03 | Dining out | Lunch with coworkers, Thai restaurant | 18.75 | 15 | Cash | Unplanned, should bring lunch tomorrow |

| 2026-03-03 | Subscriptions | Spotify Premium monthly | 10.99 | 10.99 | Credit card | Auto-renewal |

| 2026-03-03 | Health | Pharmacy — vitamins and cold medicine | 24.3 | 0 | Debit card | Unexpected, feeling under the weather |

How to fill in each field

Each page is a table with columns. Fill in one row per entry. Here's what each column is for:

Date

Write today's date. This anchors your entry in time and helps when reviewing entries later.

Category

Assign a category to this entry (e.g., food, transport, entertainment). Consistent categories make your data easy to analyze.

Description

Write a brief description of what this entry is about. Future-you will thank present-you for the context.

Amount

Record the amount for this entry. Be precise — rounding creates inaccuracies that add up over time.

Planned

Payment method

Notes

Add any additional context or thoughts. This catch-all column is for anything that doesn't fit elsewhere but might be useful later.

Tips for success

When and how often to write

Log every expense the moment it happens, or at minimum during a 5-minute evening review. The key is daily consistency — even one skipped day creates gaps that snowball into abandonment. At the end of each week, total your categories and compare to the previous week. Monthly, review category totals against your budget targets and identify the top three areas where actual spending deviated most from your plan.

Frequently Asked Questions

Why use a paper expense journal when apps like Mint or YNAB exist?

Three reasons. Handwriting an expense creates an awareness moment — Soman (2001, Journal of Consumer Research, 27(4), 460–474) showed that more 'painful' payment recording reduces later spending. Privacy: account aggregators and budgeting apps access your full transaction history. Third, apps automate tracking, but the manual pause is what changes behavior. Many users run paper and digital in parallel.

What expense categories should I use in my budget?

The U.S. Bureau of Labor Statistics Consumer Expenditure Survey (2024) reports average household allocations: housing (~33%), transportation (~17%), food (~12%), personal insurance and pensions (~12%), healthcare (~8%), entertainment (~5%), apparel (~3%). For personal budgets, 7–10 categories suffice: groceries, dining out, transport, utilities, communications, entertainment, clothing, health, gifts, other. Keep categories fixed — month-over-month comparison requires stable definitions.

What is the envelope method and does it work with a paper journal?

Cash stuffing (envelope budgeting) was popularized by Dave Ramsey in The Total Money Makeover (Thomas Nelson, 2003). Its academic foundation is Heath & Soll (1996, Journal of Consumer Research, 23(1), 40–52): mental categorization of budget ('mental budgeting') significantly reduces overspending. At month start, cash is allocated across category envelopes; spending happens only from them. Journal and envelopes reinforce each other.

How do I use the planned-vs-actual comparison in this expense journal?

At month start, record your planned amount per category in the 'planned' column. Log actuals as you spend. Weekly and monthly, compute the variance. Zero-based budgeting (Pyhrr, 1970, Harvard Business Review, Nov–Dec) requires every budget unit to have an assignment. If actuals exceed plan by more than 15% in a category, revise either the plan or the spending habits.

How many entries fit on one page of the expense journal?

18 lines per day — enough for most households. The Federal Reserve's Survey of Consumer Payment Choice (2022) reports U.S. consumers average 39 transactions per month, roughly 1.3 per day. High-frequency households reach 6–8 daily. The template provides 32 pages: 30 days plus cover and instructions. For many small same-type purchases, group them into one line with a total.

How do I analyze my expense journal at the end of the month?

Five steps: 1) sum totals by category; 2) identify the top 3 categories by share; 3) flag plan-vs-actual variances above 15%; 4) tally impulse purchases on a separate line; 5) commit to 1–2 adjustments next month. Monthly expense review is a standard recommendation of the U.S. Consumer Financial Protection Bureau (CFPB) and similar financial-literacy programs from national central banks.

Is this expense journal suitable for family budgets or only personal?

Both. For family use, add the spender's initials in the 'notes' column. Archuleta et al. (2011, Journal of Family and Economic Issues, 32(4)) found that joint financial planning correlates with higher marital satisfaction and lower financial conflict. Alternative: two journals with a 30-minute weekly reconciliation. Either way, shared visibility of spending eliminates hidden expenses.

Is it true that card spending exceeds cash spending?

Yes, and it has been confirmed repeatedly. The first study was Hirschman (1979, Journal of Consumer Research, 6(1), 58–66). Soman (2001, JCR, 27(4)) measured significantly higher card spending in supermarkets. Prelec & Simester (2001, Marketing Letters, 12(1), 5–12) ran an MIT auction experiment showing willingness-to-pay up to 100% higher with cards. The payment method column lets you test this pattern in your own data over a month.

You Might Also Like

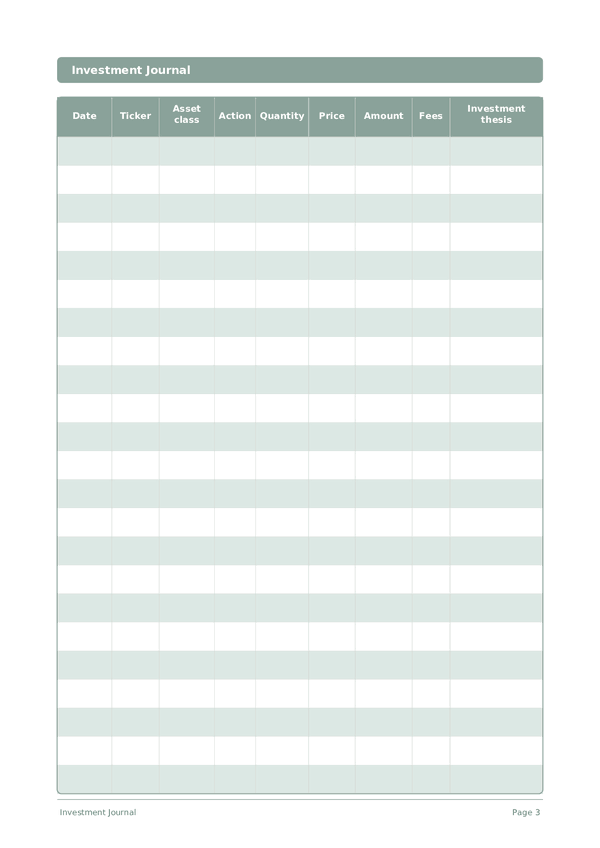

Investment Journal

Track trades, analyze decisions, and grow your portfolio

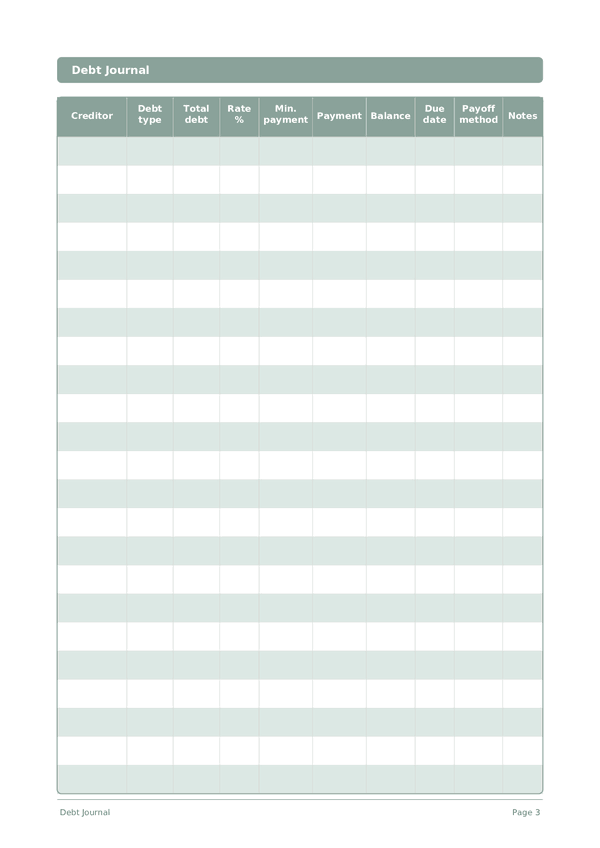

Debt Journal

Track and eliminate debt with a clear payoff strategy

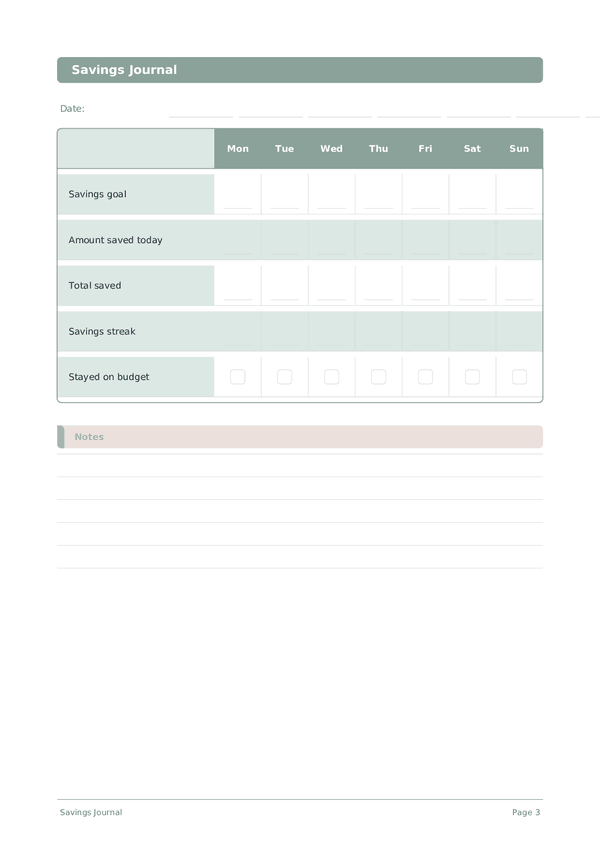

Savings Journal

Track daily savings habits and build toward your financial goals

Career Journal

Track achievements and accelerate professional growth every day

Scroll to zoom, drag to move