Printable Diario dei Debiti

Monitora ed elimina i debiti con una chiara strategia di rimborso

Personalizza campi

Attiva o disattiva i campi. Clicca la matita per rinominare, oppure aggiungi i tuoi campi.

Cos'è questo diario?

Questo è un diario a registro tabellare — ogni pagina contiene una tabella strutturata con colonne per registrare i dati. Perfetto per tenere traccia di spese, allenamenti, letture o qualsiasi attività che beneficia di voci organizzate e confrontabili.

Come compilare ogni campo

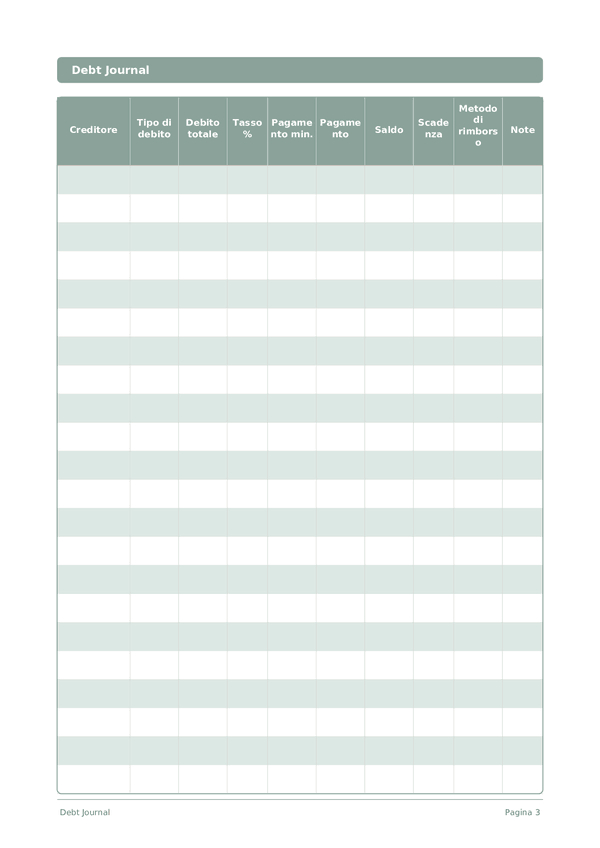

Ogni pagina è una tabella con colonne. Compila una riga per ogni voce. Ecco a cosa serve ogni colonna:

Creditore

Tipo di debito

Debito totale

Tasso %

Pagamento min.

Pagamento

Saldo

Scadenza

Metodo di rimborso

Note

Aggiungi qualsiasi contesto o pensiero aggiuntivo. Questa colonna tuttofare è per tutto ciò che non si adatta altrove ma potrebbe essere utile in seguito.

Consigli per il successo

Quando e con quale frequenza scrivere

Aggiungi voci man mano che gli eventi accadono durante il giorno. Per i registri finanziari, annota ogni transazione immediatamente. Per i registri di attività, compila dopo ogni sessione. Fai una revisione settimanale o mensile per analizzare i tuoi dati ed estrarre intuizioni.

Domande frequenti

Come differiscono il metodo snowball e quello avalanche nella colonna metodo rimborso?

Lo snowball ordina i debiti a partire dal saldo più piccolo; l'avalanche parte dal tasso interesse più alto. Dave Ramsey ha reso popolare lo snowball in 'The Total Money Makeover' (Thomas Nelson, 2003) per il suo slancio motivazionale. L'avalanche minimizza matematicamente il totale degli interessi pagati. Il CFPB (2023, 'How to Pay Off Credit Card Debt') descrive entrambe come strategie legittime; la colonna metodo rimborso di questo diario ti permette di segnare e rispettare la scelta fatta per ogni creditore.

Come compilo correttamente la colonna tasso interesse?

Usa il tasso annuo effettivo globale (TAEG) indicato nel tuo estratto conto, non il tasso mensile. Il CFPB (2023, 'What is a credit card interest rate?') definisce il TAEG come il costo annuo standardizzato del credito. Inserisci lo stesso formato per ogni creditore in modo che i confronti siano validi. Per le carte a tasso variabile, aggiorna la colonna quando il tasso cambia — tipicamente dopo le decisioni delle banche centrali.

Perché il diario include sia la colonna pagamento minimo sia quella pagamento?

Il pagamento minimo è ciò che il creditore richiede; il pagamento è ciò che paghi effettivamente. Il CFPB (2022, 'Making Minimum Payments on Credit Cards') avverte che pagare solo il minimo può prolungare il rimborso di anni e raddoppiare il totale degli interessi. Monitorare entrambe le colonne affiancate mostra il divario e motiva ad aumentare il pagamento ogni volta che è possibile per accelerare l'estinzione del debito.

Il metodo avalanche è davvero matematicamente migliore?

L'avalanche minimizza il totale degli interessi matematicamente perché punta prima al tasso interesse più alto. Il CFPB (2023, 'How to Pay Off Credit Card Debt') osserva che entrambi i metodi funzionano e che la scelta giusta dipende dal fatto che tu abbia bisogno di motivazione o di risparmio. Lo snowball spesso vince dal punto di vista comportamentale per chi ha bisogno di successi iniziali per mantenersi costante — registra il tuo metodo e rispettalo.

Come tengo traccia del saldo progressivo su più pagine?

Usa la colonna saldo dopo ogni pagamento: saldo precedente meno pagamento, più eventuali interessi maturati nel periodo. Il CFPB (2023, 'Understanding Your Credit Card Statement') spiega come gli interessi vengano aggiunti al capitale non pagato ogni ciclo. Con 15 righe per pagina, pianifica un creditore per riga nell'arco del mese; riporta il saldo finale come voce iniziale nella pagina successiva.

Qual è l'errore più comune nell'iniziare un diario dei debiti?

Omettere i debiti minori. Il CFPB (2022, 'Debt Collection') raccomanda di elencare ogni obbligazione — sanitaria, carte store, prestiti personali, prestiti familiari — perché i debiti nascosti mandano in crisi qualsiasi piano. Compila la colonna creditore per ogni saldo superiore a zero, anche se il pagamento minimo è piccolo. Le 15 righe per pagina si adattano al quadro debitorio completo della maggior parte delle famiglie su un unico foglio.

Scrivere i debiti aiuta davvero a motivare il rimborso?

Sì, il progresso visivo è una leva comportamentale documentata. Thaler & Sunstein, 'Nudge' (Yale University Press, 2008) descrivono il monitoraggio scritto come un dispositivo di impegno che aumenta la costanza. Il CFPB (2022, 'Tools for Tracking Your Money') approva i registri scritti per il cambiamento comportamentale. Vedere la colonna saldo diminuire riga per riga fornisce il ciclo di feedback che trasforma gli obiettivi astratti in azioni sostenute.

Dovrei includere il mutuo in questo diario?

Facoltativo — la maggior parte dei sostenitori del metodo snowball/avalanche esclude i mutui perché l'orizzonte temporale è diverso. Dave Ramsey, 'The Total Money Makeover' (Thomas Nelson, 2003) tratta la casa come una fase separata successiva. Usa la colonna tipo debito per indicare 'mutuo' e decidi. Se escludi il mutuo, concentra le 15 righe su carte di credito, prestiti auto, prestiti studenteschi e prestiti personali, dove un tasso interesse elevato rende più impattante un rimborso accelerato.

Potrebbe piacerti anche

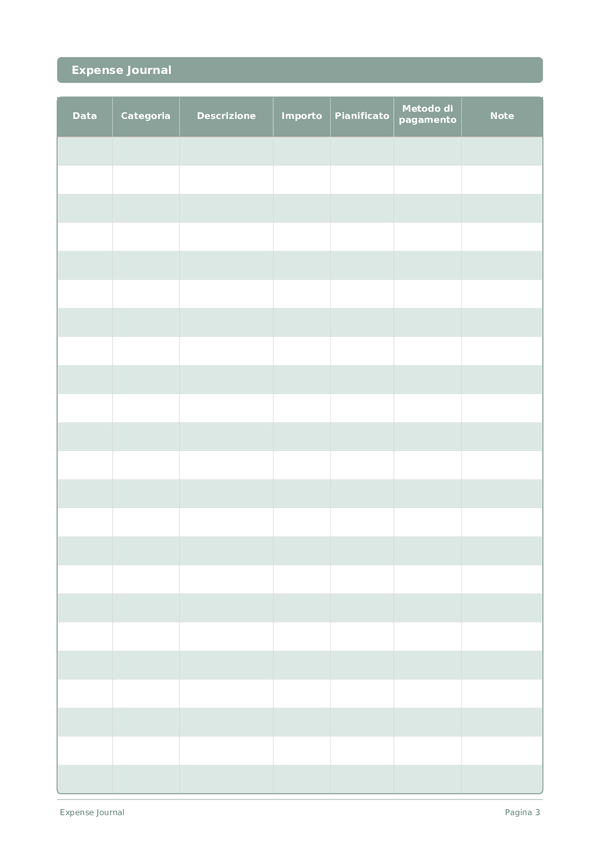

Diario delle Spese

Monitora ogni euro per prendere il controllo delle tue finanze

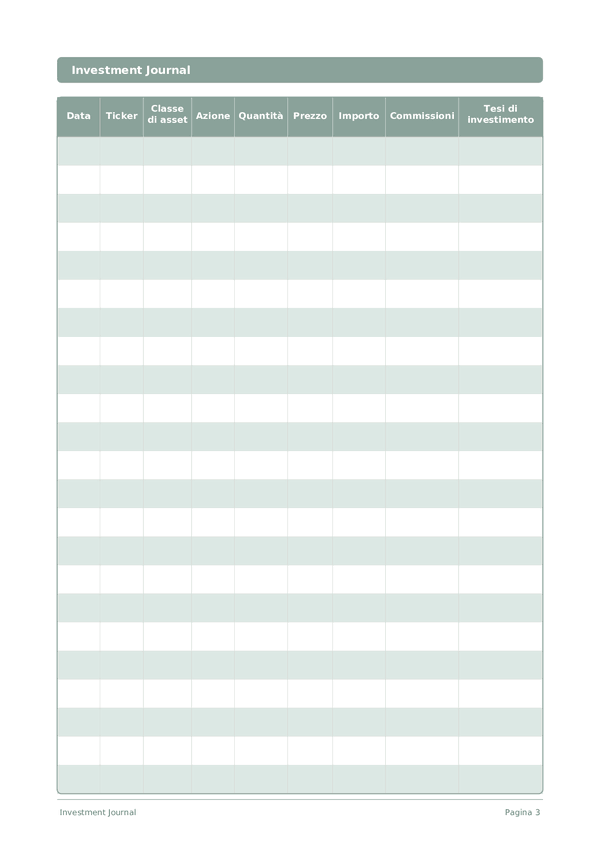

Diario degli Investimenti

Monitora le operazioni, analizza le decisioni e fai crescere il tuo portafoglio

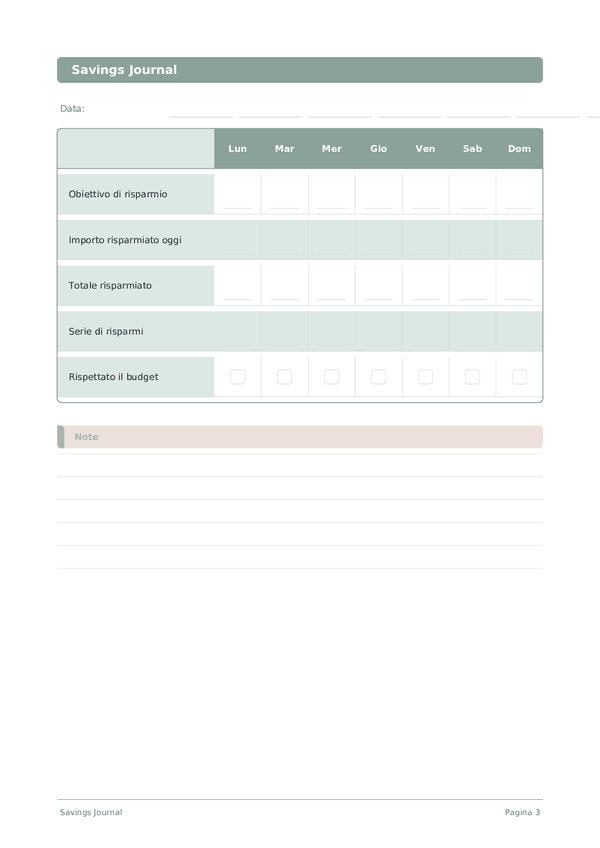

Diario del Risparmio

Monitora le abitudini di risparmio quotidiane e avanzati verso i tuoi obiettivi finanziari

Diario di Carriera

Monitora i risultati e accelera la crescita professionale ogni giorno

Scorri per ingrandire, trascina per spostare