Printable Debt Journal

Track and eliminate debt with a clear payoff strategy

Track every debt, interest rate, and payment in one structured table. Log your creditor, debt type, and chosen payoff strategy — snowball or avalanche — to stay organized and accelerate your path to financial freedom.

Customize fields

Toggle fields on or off. Click the pencil to rename, or add your own fields.

Benefits

How to Use

What is this journal?

A debt journal is a structured tracking tool for anyone working to pay off loans, credit cards, or other financial obligations. By recording each creditor, debt type, total owed, interest rate, minimum payment, actual payment made, remaining balance, and your chosen payoff method, you maintain complete visibility over your debt landscape. This journal transforms the often overwhelming experience of carrying multiple debts into a clear, manageable action plan.

Debt payoff is as much a psychological challenge as a financial one. Seeing your balances decrease — even by small amounts — provides the motivation to keep going. This journal supports popular payoff strategies like the debt snowball (paying off smallest balances first for quick wins) and debt avalanche (tackling highest interest rates first for mathematical efficiency), helping you stay committed to whichever approach suits your personality and situation.

Whether you are managing student loans, a mortgage, credit card balances, medical bills, or personal loans, this journal keeps every obligation organized in one place. It is particularly powerful when paired with a budget journal, as together they ensure that every extra dollar is strategically directed toward your most impactful debt, accelerating your path to financial freedom.

Filled example

Here's what a typical entry looks like when filled in:

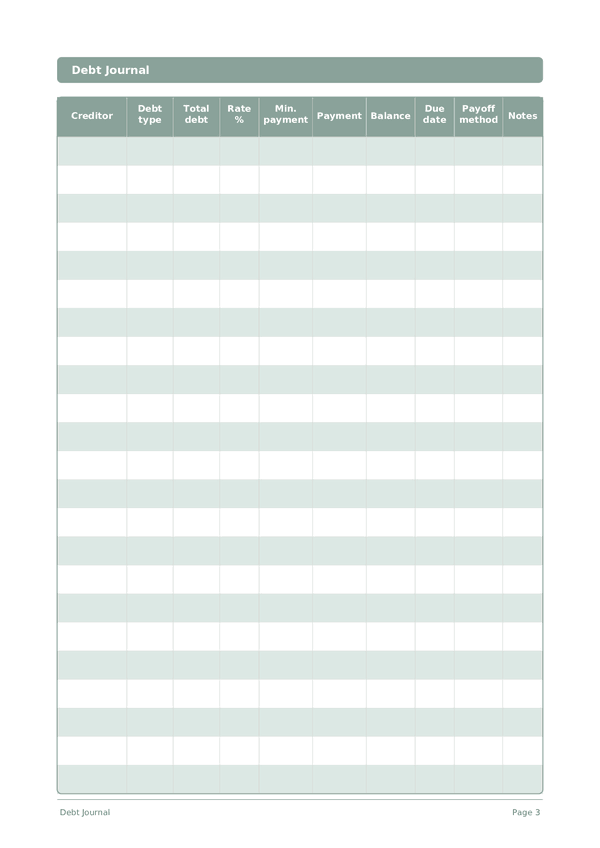

| Creditor | Debt type | Total debt | Rate % | Min. payment | Payment | Balance | Due date | Payoff method | Notes |

|---|---|---|---|---|---|---|---|---|---|

| Chase Visa | Credit card | 4200 | 22.99 | 84 | 350 | 3850 | 2026-03-15 | Avalanche | Highest interest — priority target |

| Sallie Mae | Student loan | 18500 | 5.5 | 195 | 195 | 18305 | 2026-03-28 | Standard | Federal loan, income-driven repayment |

| Toyota Financial | Auto loan | 12800 | 4.25 | 310 | 310 | 12490 | 2026-03-20 | Standard | 24 months remaining |

| Capital One | Credit card | 1150 | 19.99 | 35 | 200 | 950 | 2026-03-10 | Snowball | Smallest balance — close to payoff! |

| City Hospital | Medical bill | 2400 | 0 | 100 | 100 | 2300 | 2026-03-25 | Standard | 0% interest payment plan, 24 months |

How to fill in each field

Each page is a table with columns. Fill in one row per entry. Here's what each column is for:

Creditor

Debt type

Total debt

Rate %

Min. payment

Payment

Balance

Due date

Payoff method

Notes

Add any additional context or thoughts. This catch-all column is for anything that doesn't fit elsewhere but might be useful later.

Tips for success

When and how often to write

Update your debt table every time you make a payment — capturing the new balance, amount paid, and any extra above the minimum. At minimum, this happens monthly with regular payment cycles. Weekly, spend 5 minutes reviewing upcoming due dates to avoid late fees. Monthly, recalculate your total debt, total interest paid, and debt-to-income ratio. Celebrate each debt fully paid off with a journal entry reflecting on what you learned and how it felt.

You Might Also Like

Expense Journal

Track every dollar to take control of your finances

Investment Journal

Track trades, analyze decisions, and grow your portfolio

Savings Journal

Track daily savings habits and build toward your financial goals

Career Journal

Track achievements and accelerate professional growth every day