Printable Journal des dettes

Suivez et éliminez vos dettes avec une stratégie de remboursement claire

Track every debt, interest rate, and payment in one structured table. Log your creditor, debt type, and chosen payoff strategy — snowball or avalanche — to stay organized and accelerate your path to financial freedom.

Personnaliser les champs

Activez ou désactivez les champs. Cliquez sur le crayon pour renommer, ou ajoutez vos propres champs.

Avantages

Comment utiliser

Qu'est-ce que ce journal ?

A debt journal is a structured tracking tool for anyone working to pay off loans, credit cards, or other financial obligations. By recording each creditor, debt type, total owed, interest rate, minimum payment, actual payment made, remaining balance, and your chosen payoff method, you maintain complete visibility over your debt landscape. This journal transforms the often overwhelming experience of carrying multiple debts into a clear, manageable action plan.

Debt payoff is as much a psychological challenge as a financial one. Seeing your balances decrease — even by small amounts — provides the motivation to keep going. This journal supports popular payoff strategies like the debt snowball (paying off smallest balances first for quick wins) and debt avalanche (tackling highest interest rates first for mathematical efficiency), helping you stay committed to whichever approach suits your personality and situation.

Whether you are managing student loans, a mortgage, credit card balances, medical bills, or personal loans, this journal keeps every obligation organized in one place. It is particularly powerful when paired with a budget journal, as together they ensure that every extra dollar is strategically directed toward your most impactful debt, accelerating your path to financial freedom.

Exemple rempli

Voici à quoi ressemble une entrée typique une fois remplie :

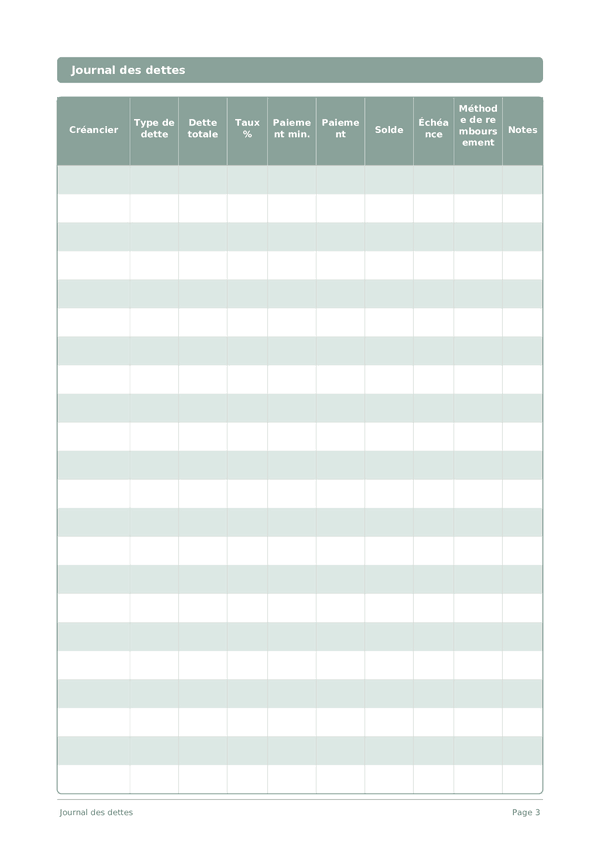

| Créancier | Type de dette | Dette totale | Taux % | Paiement min. | Paiement | Solde | Échéance | Méthode de remboursement | Notes |

|---|---|---|---|---|---|---|---|---|---|

| Chase Visa | Credit card | 4200 | 22.99 | 84 | 350 | 3850 | 2026-03-15 | Avalanche | Highest interest — priority target |

| Sallie Mae | Student loan | 18500 | 5.5 | 195 | 195 | 18305 | 2026-03-28 | Standard | Federal loan, income-driven repayment |

| Toyota Financial | Auto loan | 12800 | 4.25 | 310 | 310 | 12490 | 2026-03-20 | Standard | 24 months remaining |

| Capital One | Credit card | 1150 | 19.99 | 35 | 200 | 950 | 2026-03-10 | Snowball | Smallest balance — close to payoff! |

| City Hospital | Medical bill | 2400 | 0 | 100 | 100 | 2300 | 2026-03-25 | Standard | 0% interest payment plan, 24 months |

Comment remplir chaque champ

Chaque page est un tableau avec des colonnes. Remplissez une ligne par entrée. Voici à quoi sert chaque colonne :

Créancier

Type de dette

Dette totale

Taux %

Paiement min.

Paiement

Solde

Échéance

Méthode de remboursement

Notes

Ajoutez tout contexte ou réflexion supplémentaire. Cette colonne fourre-tout est pour tout ce qui ne rentre pas ailleurs mais pourrait être utile plus tard.

Conseils pour réussir

Quand et à quelle fréquence écrire

Update your debt table every time you make a payment — capturing the new balance, amount paid, and any extra above the minimum. At minimum, this happens monthly with regular payment cycles. Weekly, spend 5 minutes reviewing upcoming due dates to avoid late fees. Monthly, recalculate your total debt, total interest paid, and debt-to-income ratio. Celebrate each debt fully paid off with a journal entry reflecting on what you learned and how it felt.

Questions fréquentes

Quelle différence entre les méthodes boule de neige et avalanche dans la colonne méthode de remboursement ?

La boule de neige classe les dettes par solde le plus faible en premier ; l'avalanche les classe par taux d'intérêt le plus élevé. Dave Ramsey a popularisé la boule de neige dans *The Total Money Makeover* pour son élan comportemental. L'avalanche minimise la somme totale des intérêts mathématiquement. Le CFPB/Banque de France reconnaît les deux comme stratégies valides ; la colonne méthode de remboursement vous permet de choisir et de maintenir votre choix par créancier.

Comment remplir correctement la colonne taux % ?

Utilisez le taux annuel effectif global (TAEG) figurant sur votre relevé, et non le taux mensuel. Le TAEG est la mesure standardisée du coût annuel d'emprunt. Entrez la même forme pour chaque créancier afin que les comparaisons soient valides. Pour les cartes à taux variable, mettez à jour la colonne lors de chaque changement de taux, généralement après les décisions de la Banque Centrale Européenne.

Pourquoi le carnet inclut-il à la fois paiement min. et payment ?

Paiement min. est ce qu'exige le créancier ; payment est ce que vous payez réellement. Payer seulement le minimum peut prolonger le remboursement de plusieurs années et doubler les intérêts totaux. Suivre les deux colonnes côte à côte montre l'écart et motive à augmenter le payment dès que possible pour accélérer le désendettement.

La méthode avalanche est-elle vraiment mathématiquement supérieure ?

L'avalanche minimise les intérêts totaux mathématiquement en ciblant d'abord le taux d'intérêt le plus élevé. Les deux méthodes fonctionnent et le bon choix dépend de si vous avez besoin de motivation ou d'économies. La boule de neige gagne souvent sur le plan comportemental pour les personnes ayant besoin de victoires rapides — consignez votre méthode et tenez-vous-y.

Comment suivre le solde courant sur plusieurs pages ?

Utilisez la colonne balance après chaque paiement : solde précédent moins payment, plus les intérêts courus pendant la période. Avec 15 lignes par page, prévoyez un créancier par ligne sur le mois ; reportez le solde final sur la première entrée de la page suivante.

Quelle est l'erreur la plus fréquente au démarrage d'un journal de dettes ?

Omettre les petites dettes. Le CFPB/Banque de France recommande de lister toutes les obligations — médicales, cartes magasin, prêts personnels, prêts familiaux — car les dettes cachées font dérailler tout plan. Remplissez la colonne creditor pour chaque solde supérieur à zéro, même si paiement min. est faible. La page de 15 lignes accueille la situation d'endettement complète de la plupart des ménages.

Écrire ses dettes aide-t-il vraiment à motiver le remboursement ?

Oui, la progression visuelle est un levier comportemental documenté. Thaler & Sunstein, *Nudge* (2008), décrivent le suivi écrit comme un dispositif d'engagement qui augmente le respect des plans. Le CFPB/Banque de France approuve les journaux écrits pour le changement de comportement financier. Voir la colonne balance diminuer ligne par ligne fournit la boucle de rétroaction qui transforme des objectifs abstraits en actions soutenues.

Dois-je inclure mon prêt immobilier dans ce carnet ?

C'est optionnel — la plupart des praticiens boule de neige/avalanche excluent l'immobilier car l'horizon de temps diffère. Dave Ramsey traite le logement comme une phase ultérieure séparée. Utilisez la colonne type de dette avec la mention « immobilier » et décidez selon votre situation. Si vous l'excluez, concentrez les 15 lignes sur les cartes de crédit, prêts auto, prêts étudiants et personnels où un taux élevé rend le remboursement rapide impactant.

Vous aimerez aussi

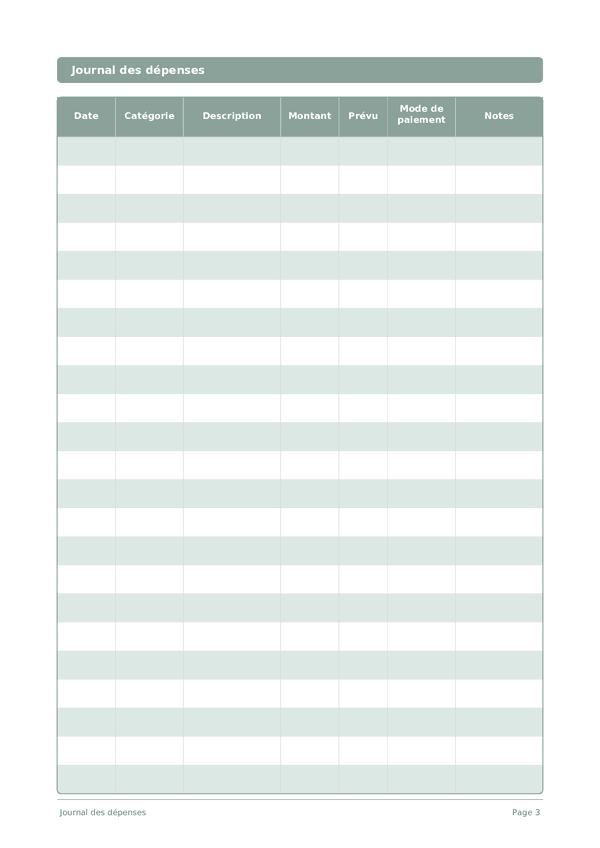

Journal des dépenses

Suivez chaque euro pour prendre le contrôle de vos finances

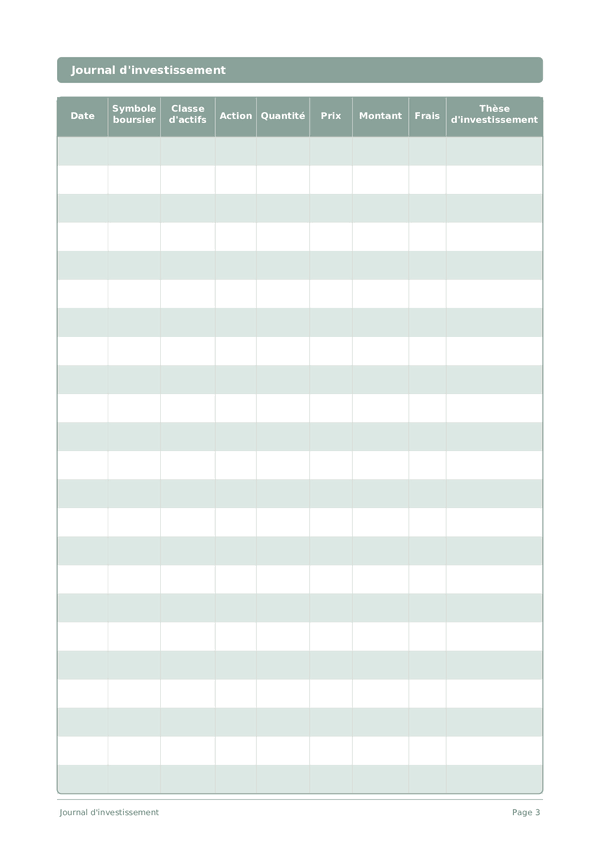

Journal d'investissement

Suivez vos transactions, analysez vos décisions et faites croître votre portefeuille

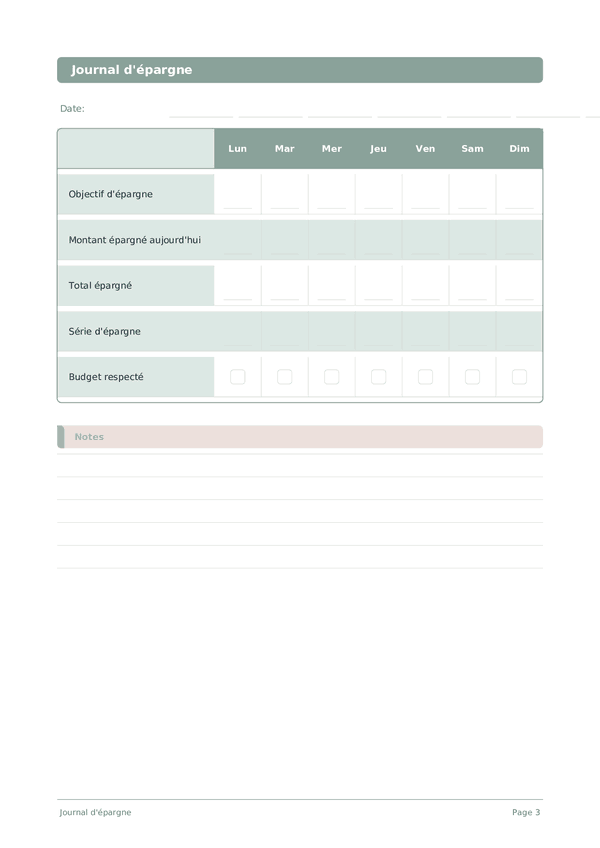

Journal d'épargne

Suivez vos habitudes d'épargne quotidiennes et progressez vers vos objectifs financiers

Journal de carrière

Suivez vos réalisations et accélérez votre croissance professionnelle chaque jour

Molette pour zoomer, glisser pour déplacer